If your employer has decided to offer you equity compensation, you’re already in a strong position. This benefit, typically offered as company stock shares, is usually reserved for valued team members the company wants to retain. While equity compensation can meaningfully boost your savings and help you reach your financial goals, it requires careful planning. There are several types of equity compensation, each with its own terms and tax implications. So, if you’re receiving (or about to receive) equity compensation, it’s essential to understand the specific details of your plan.

Equity compensation packages don’t come with a manual. Most companies don’t have in-house experts who can offer personal financial advice or help you manage your grant. They can explain how the program works but cannot provide customized planning recommendations. As more employers adopt equity-based compensation, understanding how these plans function is more important than ever. In this article, we’ll review two of the most common types: incentive stock options (ISOs) and restricted stock units (RSUs).

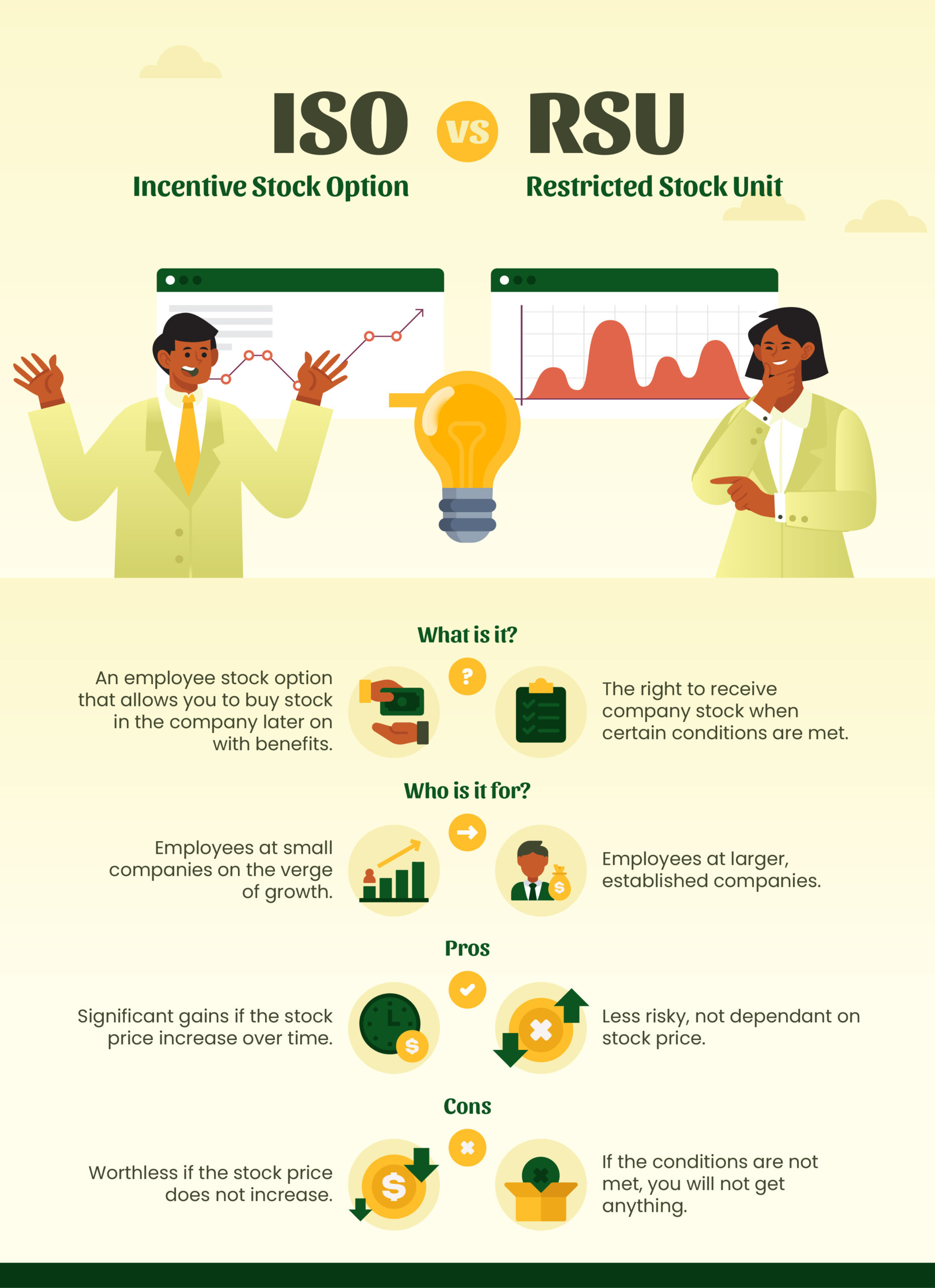

ISO vs RSU: Breaking Down the Terms

Before diving into ISOs and RSUs, it helps to understand some key terms you’ll often hear with these plans:

- Grant Date: The date the company’s board of directors formally approves the award.

- Grant Price: The stock’s fair market value on the grant date.

- Vesting: The process of earning ownership of shares over time.

- Vesting Period: The length of time over which your shares become vested, as defined in your grant agreement.

- Vesting Value: The fair market value of the shares that vest on a specific date.

- Exercise: Notifying the company that you intend to buy stock through your option.

- Exercise Price (Strike Price): The price you pay per share when you exercise your option. For example, if you can buy 500 shares at $10 each, the exercise price is $10.

- Spread: The difference between the stock’s current value and the exercise price.

What Is an ISO (Incentive Stock Option)?

An incentive stock option (ISO) is one of two main types of employee stock options (the other being non-qualified stock options, or NQSOs). An ISO allows you to purchase company stock later at the price it was worth when the option was granted. ISOs are especially common at smaller, fast-growing companies.

When you exercise an ISO, you don’t immediately owe regular income tax—but you may trigger the alternative minimum tax (AMT).

Here are some important considerations about ISOs and retirement:

- Timing of Sale: If you hold the stock for at least one year after exercising and two years after the grant date, any profits are taxed as long-term capital gains rather than regular income.

- Diversification: While ISOs can help grow wealth, they tie part of your retirement portfolio to a single company’s stock, which increases risk. Consider how they fit into your overall investment mix.

- Retirement Contributions: Exercising an ISO doesn’t create earned income for IRA or 401(k) contributions. Only W-2 or self-employment income qualifies.

- Rollover Rules: ISOs can’t be rolled into a retirement account. They must be exercised while you’re employed or within a short period—usually 90 days—after leaving the company.

Because ISOs can be complex and have significant tax consequences, it’s wise to consult a financial planner before making any decisions.

Pros and Cons of ISOs

ISOs carry risk: if the company’s stock doesn’t rise before the option expires, the option becomes worthless. However, if the stock performs well, ISOs can lead to substantial gains for employees willing to accept the risk.

What Is an RSU (Restricted Stock Unit)?

A restricted stock unit (RSU) is the simplest form of equity compensation. It represents a promise to give you company stock once certain conditions are met. RSUs are common at larger, established companies.

Typical conditions for receiving RSUs include:

- Remaining with the company for a set period

- Achieving a specific sales goal

- Completing a project by a deadline

If these conditions aren’t met, the shares are forfeited. RSUs don’t become yours until they vest, meaning you won’t receive dividends or other stockholder benefits before that time. Some employers, however, provide dividend equivalents during the vesting period.

Taxes on RSUs are generally straightforward. You don’t owe tax when the grant is awarded, but once your shares vest, their value is treated as compensation income and included on your W-2. This amount is subject to federal, state, Social Security, and Medicare tax.

Pros and Cons of RSUs

Compared to ISOs, RSUs carry less risk because they aren’t tied to the stock’s price performance. As long as the company’s stock has value when your shares vest, you’ll receive compensation. However, if you leave the company before vesting or fail to meet the required conditions, you’ll lose the shares entirely.

ISO vs. RSU: Which Is Better for Retirement?

Both ISOs and RSUs offer unique advantages and drawbacks. Neither is inherently better—it depends on your financial goals, risk tolerance, and overall retirement plan.

When evaluating your options, ask yourself:

- How do these stock awards fit into my long-term goals?

- What level of risk am I comfortable taking?

- How will these shares impact my tax situation?

- Should I hold the shares, sell them, or consider a cashless exercise?

As equity compensation becomes more common, it’s essential to understand not only what type you’re receiving but also how it affects your taxes and long-term strategy. Integrating equity compensation into your broader financial plan helps ensure you’re managing both risk and opportunity wisely.

If your company offers you equity compensation, take time to discuss it with your financial planner. They can help you understand how your stock options fit into your overall wealth and retirement plan.

For more answers to common retirement questions, read our Comprehensive Guide to Retirement Planning in New Jersey.